When we think about generational phenomenon, what usually comes to mind? Well, for me, I think about things like Microsoft and Bill Gates putting a computer in every home or Jeff Bezos transforming retail from brick and mortar to essentially on-demand delivery with a click of the mouse. We think of these as a generational phenomenon because these types of changes to the way we communicate, work, live, and shop only used to happen every 20 to 30 years. With the growing rate of technological advances, however, these phenomena are happening at a much faster rate. What used to take decades now only takes 5 years. Look at Uber for example. If you would have told me in 2011 that by 2016 taxi cabs would be basically obsolete, I would have told you that you were crazy. However, as it turns out, because of the way we are all connected now, this type of change happens incredibly fast.

While Bitcoin is in itself a generational phenomenon as described above, this article intends to show you that the real phenomenon in regards to Bitcoin is just beginning, and it is fact generational, just in a different context of the word. Recently, Warren Buffet was on CNBC and when asked about Bitcoin and cryptocurrency, he offered the following remarks “Cryptocurrencies basically have no value,” and “I don’t own any cryptocurrency, I never will…You can’t do anything with it except sell it to someone else.” Another famous Bitcoin and cryptocurrency skeptic is Mark Cuban. He recently said, “I’d rather have bananas than Bitcoin.” If you are a person who follows finance, you will most definitely know and respect what Mr. Buffet and Mr. Cuban have accomplished in their respective financial lives. Their opinions DO matter on this kind of thing. So why are they so negative on Bitcoin, what do they see that we don’t? Well, the answer to that question can be answered in a very simple statement: They don’t care.

Warren Buffet is a member of the Silent Generation, while Mark Cuban is a member of the Baby Boomer Generation. Both men were the beneficiaries of a government policy in which individuals could borrow money at an increasingly lower interest rate for the entirety of their business careers. Until 2008 in fact, most people could go to a bank and get a loan, assuming they had a heartbeat. If you wanted to start a business or go buy real estate getting money was relatively easy. The reason that it was easy is too long of a topic for this article to cover, just know that in relation to Millennials and Gen Z readers, obtaining a loan was exponentially easier for the Silent Generation and Boomers. (I want to be clear here, both Mr. Buffet and Mr. Cuban have worked their ass off and deserve all the success they have gained, their success was contingent on much more than being able to obtain easy money.) The ability to get a loan and access to capital is one of the biggest barriers individuals have to start a business or investing. So, from the perspective of Mr. Buffet and Mr. Cuban, the system has worked just fine. Why would anyone want to change it?

The answer for most successful people in the Silent Generation and Baby Boomer Generation is that we wouldn’t change it. Their wealth is denominated in the fiat currency USD, for the most part, and that has worked just fine. Here is where things get interesting and why I believe Mr. Buffet and Mr. Cuban have Bitcoin wrong. If we zoom out, we see that since 1971 the United States Dollar was taken off of the gold standard. This has resulted in unprecedented money printing over the last 50 years that is now just starting to catch up to the economy. Who does this affect? Certainly not the Silent Generation and the Baby Boomers who were the direct beneficiary of trillions of dollars being pumped into the system. Up until recently, politicians and governments have been able to just kick the debt can down the road to be dealt with at a later point in time. The problem with this is that at some point, the can turn into an anvil. At some point, this problem has to be dealt with.

What have we millennials learned from watching our parent’s behaviors in relation to money over the past 20–35 years? We have learned how to go into debt. Rough numbers suggest that 60% of millennials have debt averaging around $30,000, not including mortgages. Not a big deal right? Well, unfortunately for us, getting a loan isn’t as easy as it used to be. Ask any Millennial who has tried to apply for a home loan with student debt or tried to get a business off the ground while carrying that debt. They will tell you categorically that the banks are awful to work with. Essentially what it boils down to is that a bank will give you whatever money you have available as collateral. Essentially, you are borrowing your own money and paying interest to the bank. So, back to Mr. Buffet and Mr. Cuban, they have no problem getting capital, the system works for them because, in essence, they already have the money. They have absolutely zero incentive for anything to change at all. Millennials, however, are starting to wake up to the fact that this system is not working for us.

Now what happens from here, do we start a generational war and start blaming each other for the financial problems we face as a nation? We most certainly could, but we won’t, and here is why Bitcoin is a generational phenomenon. I don’t know the numbers, but I’d be willing to bet 99% of the Silent Generation have retired. With 47% of Baby Boomers already ready and numbers approaching 10,000 a day continuing to retire, we can start to notice something interesting happening. Firstly, all of the Baby Boomers retiring at approximately the same time potentially represents a potential problem for the stock market as they all cash in their 401k’s and holdings to live out their golden years. (This is actually an entire theory worth looking into that could potentially cause a very real problem, we just aren’t concerned with it for the purpose of this article.) Second, as Baby Boomers retire and pass their savings and businesses down to their children, Millennials, we notice that the landscape for where those potential dollars are being invested has changed.

The Silent Generation and Baby Boomer Generation did not grow up around computers. Their wealth was generated mostly in a time where the email was the most revolutionary breakthrough since color TV. Investing in Bitcoin, or any other Digital Asset for that matter, from their perspective, isn’t even something on their radar. Just like 20 years ago hopping in a strangers car and paying them through your phone would have never entered your mind. So not only are Mr. Buffet and Mr. Cuban not incentivized for things to change, they flat out don’t understand what is actually going on. (I’ll put a caveat here, I’m not saying they don’t understand Bitcoin, I’d be willing to bet they most certainly do understand it, especially Cuban, what I’m saying they don’t understand is the generational shift in investment and the emergence of digital assets as an investment class.) So what is actually going on?

We are in the middle of the greatest transfer of wealth humankind has ever seen. Baby Boomers are set to transfer $68 Trillion in wealth over the next 30 years. Yes, you read that right Trillion with a T. Where is that money going to go? That money is going to Millennial, Gen Z, Gen Y, and so on generations. These generations have spent the majority of their life on a computer. It is where we learned to work, socialize, play, learn, and connect. To us, having our money on a computer or phone is second nature. Why wouldn’t our money live on the internet? That’s where we live. What Mr. Buffet and Mr. Cuban fail to understand is that while Bitcoin and Cryptocurrency may have no value to them, it represents an entirely new financial opportunity for the rest of us who haven’t “made it.” Don’t believe me, let’s take a look at Square’s recent numbers in relation to its total revenue.

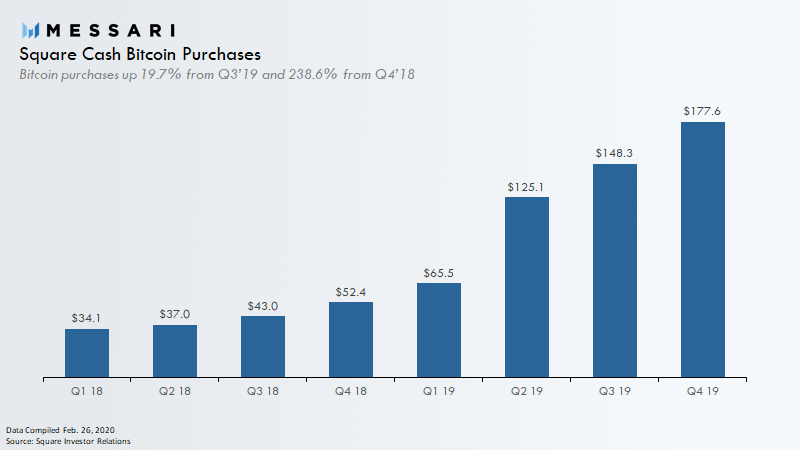

For those of you that don’t know, Square launched an app called Cash App in 2013. Cash App is a mobile transfer service allowing users to transfer money to one another using a mobile app. You just connect your bank account and find your friends and boom you can transfer money instantly. While there are similar apps out there such as Venmo that allow you to do the same thing, there is one major difference that makes square interesting to us for this article. You guessed it, Bitcoin. In November of 2017, Square announced it would start allowing its users to purchase Bitcoin through the app. Are you ready for some fun? Let’s look at the average demographic information for users of Venmo. (Unfortunately, I was unable to locate this for Cash App, but we can assume it’s fairly similar.) Venmo has approximately 40 million users each month, with Cash App approaching 15 million. (These numbers are most likely higher at the time of this writing.) Over 50% of Venmo users fall into the age range of 18–34. In Q1 of 2016, Venmo payments were 3.9 Billion. As of Q4 in 2019, Venmo payments were 29 Billion. Remember how long it took to kill the taxi? To millennials, sending money over the internet just makes sense. Now, let’s look at Bitcoin purchases on the Cash App.

In Q1 of 2018, purchases of Bitcoin on the Cash App totaled $34.1 Million. In Q4 of 2019, the purchase of Bitcoin on the Cash app rose to $177.6 Million representing more than half of Square’s quarterly revenue. Now, if you take into consideration that the majority of people using these apps are from the Millennial generation, and younger AND that the numbers using these apps continue to grow every quarter AND that as soon as competitors see how much Cash App is generating by selling Bitcoin, they won’t have a choice but to offer it just to stay competitive, AND the fact that there will only be 21 million Bitcoin ever in existence well, I hope you see where I am going with this.

Back to the greatest wealth transfer in human history. Again, over the next 30 years, Baby Boomers are going to transfer $68 Trillion with a T to the younger generations. The younger generations who have a hard time getting a loan at a bank, don’t trust the banks will take care of their money and who has spent the majority of their waking lives in front of a computer. Let us not forget, this is not only happening in the United States but all over the planet. If we look at the total market cap of Bitcoin in relation to other asset classes, we start to get a better idea of the staggering amount of growth Bitcoin and Digital Assets have in front of them.

At the time of writing this article, the entirety of the digital asset/cryptocurrency market cap including Bitcoin is $250 Billion. When Compared to gold at $7 Trillion with a T and the NYSE, which is only one equity market, at $23.1 Trillion with a T, we should be having our HOLY SHIT moment right about now. As the Baby Boomers pass their wealth down, that wealth is going to move away from traditional equity markets and assets into an asset class we are only now just beginning to see the potential of, Digital Assets. Will all of that wealth go into Digital Assets? Absolutely not. However, as we have seen the shift is already happening. I see no reason that the users of apps like Cash App will slow down anytime in the near future. More and more Millennials are starting to wake up to the fact that what worked for our parents and grandparents, will not work for us. We need to take charge and be responsible for our own fiscal well being. For many of us, Bitcoin is the opportunity to save and accumulate wealth. With a fixed supply and predictable inflation schedule, combined with the familiarity of the internet, computers, and phones…Bitcoin for Millennials and younger, is most definitely turning out to be a Generational Phenomenon, regardless of whether or not Mr. Buffet or Mr. Cuban understand or like it.

All the Best.